Showing posts with label Credit Card Interest. Show all posts

Showing posts with label Credit Card Interest. Show all posts

Credit Card Interest

Calculation of interest rates

Most U.S. credit cards are quoted in terms of nominal annual percentage rate (APR) compounded daily, or sometimes (and especially formerly) monthly, which in either case is not the same as the effective annual rate (EAR). Despite the "annual" in APR, it is not necessarily a direct reference for the interest rate paid on a stable balance over one year. The more direct reference for the one-year rate of interest is EAR. The general conversion factor for APR to EAR is , where

, where  represents the number of compounding periods of the APR per EAR period.

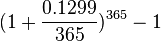

For a common credit card quoted at 12.99% APR compounded daily, the

one-year EAR is

represents the number of compounding periods of the APR per EAR period.

For a common credit card quoted at 12.99% APR compounded daily, the

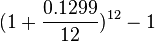

one-year EAR is  , or 13.87%; and if it is compounded monthly, the one-year EAR is

, or 13.87%; and if it is compounded monthly, the one-year EAR is  or 13.79%. On an annual basis, the one-year EAR for compounding monthly

is always less than the EAR for compounding daily. However, the

relationship of the two in individual billing periods depends on the APR

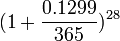

and the number of days in the billing period. For example, given 12

billing periods a year, 365 days, and an APR of 12.99%, if a billing

period is 28 days then the rate charged by monthly compounding is

greater than that charged by daily compounding (

or 13.79%. On an annual basis, the one-year EAR for compounding monthly

is always less than the EAR for compounding daily. However, the

relationship of the two in individual billing periods depends on the APR

and the number of days in the billing period. For example, given 12

billing periods a year, 365 days, and an APR of 12.99%, if a billing

period is 28 days then the rate charged by monthly compounding is

greater than that charged by daily compounding ( is greater than

is greater than  ). But for a billing period of 31 days, the order is reversed ( is less than

). But for a billing period of 31 days, the order is reversed ( is less than  ).

In general, credit cards available to middle-class cardholders that

range in credit limit from $1,000 to $30,000 calculate the finance

charge by methods that are exactly equal to compound interest

compounded daily, although the interest is not posted to the account

until the end of the billing cycle. A high U.S. APR of 29.99% carries an

effective annual rate of 34.96% for daily compounding and 34.48% for

monthly compounding, given a year with 12 billing periods and 365 day.

).

In general, credit cards available to middle-class cardholders that

range in credit limit from $1,000 to $30,000 calculate the finance

charge by methods that are exactly equal to compound interest

compounded daily, although the interest is not posted to the account

until the end of the billing cycle. A high U.S. APR of 29.99% carries an

effective annual rate of 34.96% for daily compounding and 34.48% for

monthly compounding, given a year with 12 billing periods and 365 day.Table 1 below, given by Prosper (2005), shows data from Experian, one of the 3 main U.S. and UK credit bureaus (along with Equifax in the UK and TransUnion in the U.S. and internationally). (The data actually come from installment loans [closed end loans], but can also be used as a fair approximation for credit card loans [open end loans]). The table shows the loss rates from borrowers with various credit scores. To get a desired rate of return, a lender would add the desired rate to the loss rate to determine the interest rate. Though individual borrowers differ, lenders predict that, as an aggregate, borrowers will tend to exhibit the same payment behavior that others with similar credit scores have shown in the past. Banks then compete on details by making analyses of how to use data such as these along with any other data they gather from the application and history with the cardholder, to determine an interest rate that will attract borrowers by remaining competitive with other banks and still assure a profit. Debt-to-income ratio (DTI) is another important factor for determining interest rates. The bank calculates it by adding up the borrower's obligated minimum payments on loans, and dividing by the cardholder's income. If it is more than a set point (such as 20% in this example) then loans to that applicant are considered a higher risk than given by this table. These loss rates already include incomes the lenders receive from payments in collection, either from debt collection efforts after default or from selling the loans to third parties for further collection attempts, at a fraction of the amount owed.

Subscribe to:

Posts (Atom)